A measured core place, sized with discipline, for a hygiene champion now sharpening toward its best assets.

No constitutional fortress — only one of Sweden's most patient owners and the world's #1 incontinence franchise.

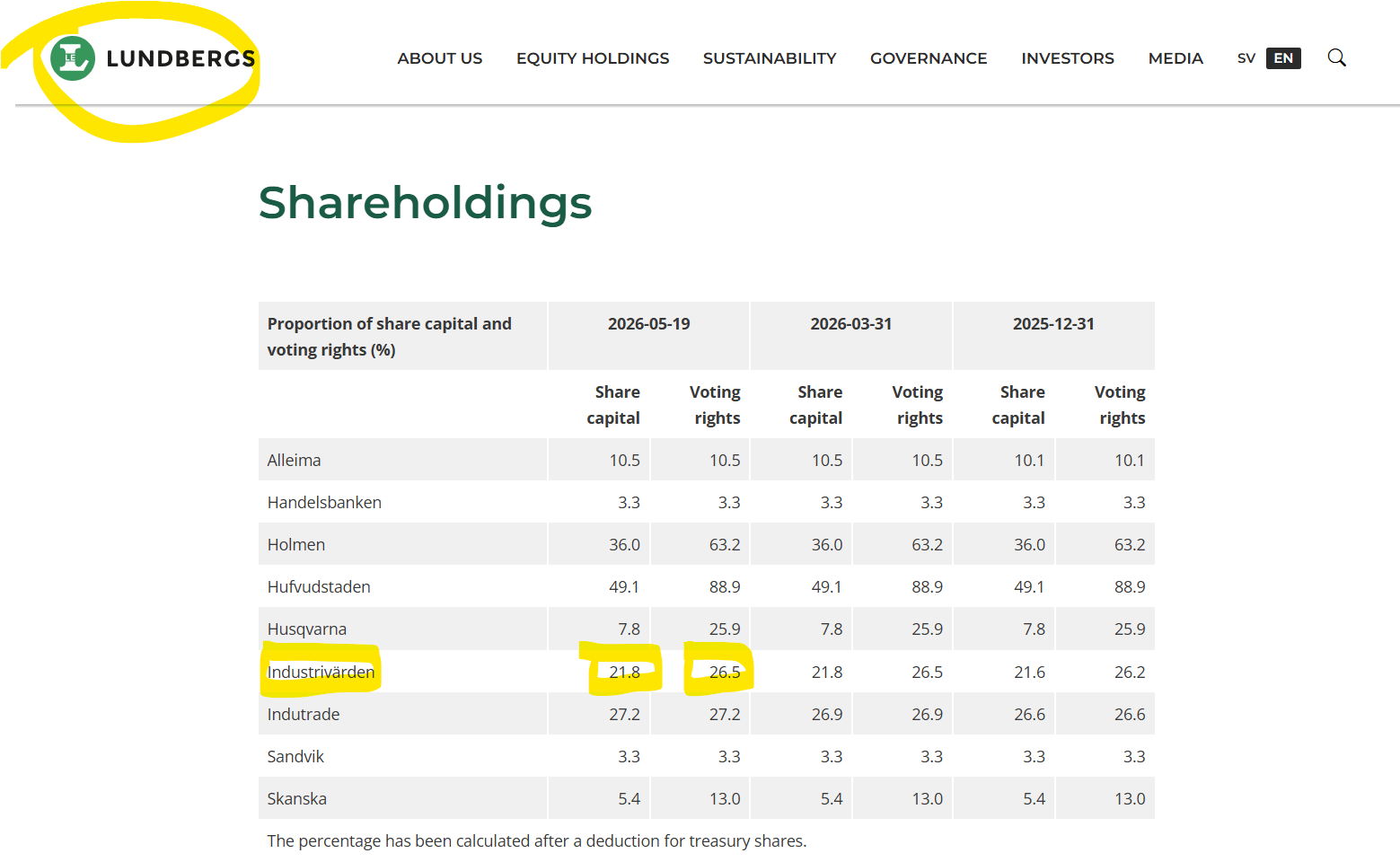

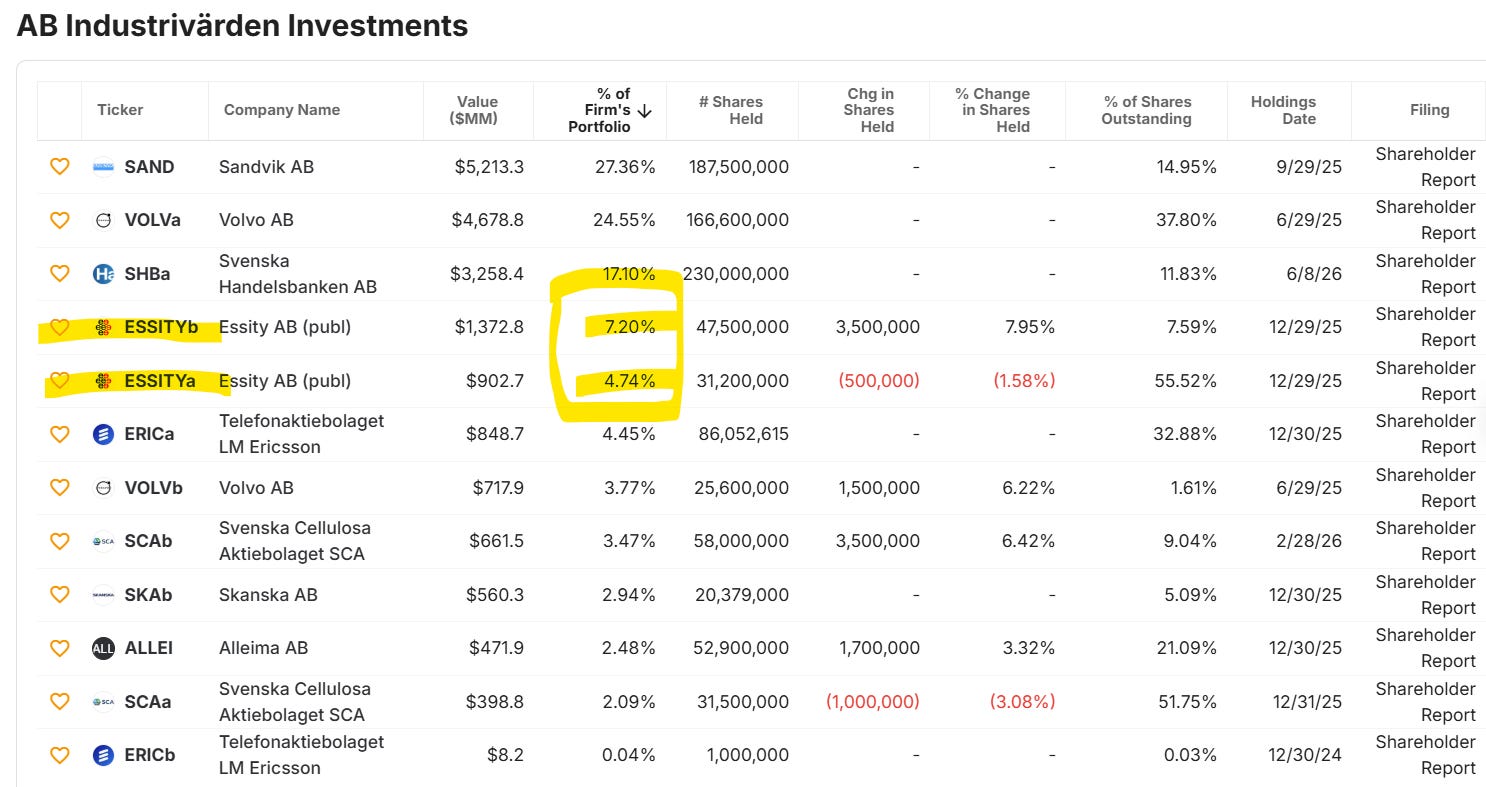

Essity is a high-quality global hygiene and health franchise wrapped in a governance structure that is respectable. It is not family- or foundation-controlled in the direct sense the framework rewards. Control runs through the Industrivärden/Lundberg sphere - a minority voting anchor, not a permanence structure. Strong business, strong balance sheet, weak constitutional moat. This is a Custodial Candidate / Tier B profile, not a Tier A foundation play. The redeeming feature is the Lundberg ownership ethos two layers up; the disqualifying feature is that nothing constitutionally prevents loss of control.

What is AB Industrivarden and who owns it?

Origins and wealth:

The family fortune originates with Lars Erik Lundberg (1920–2001), who started a small construction company in Norrköping in 1944 that evolved into L E Lundbergföretagen.

Early on, he shifted from pure contracting into owning and managing properties, building a recurring cash‑flow base and gradually reducing reliance on cyclical construction.

From the late 1970s and 1980s, the group broadened into financial assets, acquiring stakes in listed Swedish companies and transitioning from an operating construction firm into a diversified investment company.

Today, the core wealth sits in the listed holding company L E Lundbergföretagen AB, which controls Lundbergs Fastigheter (real estate) and significant equity stakes in Industrivärden, Handelsbanken, Sandvik, Skanska, Alleima and others.

Key individuals:

Lars Erik Lundberg: Founder; built the business from a small construction outfit into an integrated property and investment group.

Fredrik Lundberg (b. 1951): Lars Erik’s son, Swedish businessman and billionaire, now president and CEO of L E Lundbergföretagen and the family’s chief capital allocator. He inherited a controlling stake and has compounded it through conservative leverage, real‑estate development, and long‑term stakes in listed companies.

Next generation: His daughters, including Louise Lindh and Katarina Martinson, are involved in the family’s business sphere and associated boards (e.g. Industrivärden), forming the emerging third generation of active owners, though Fredrik remains the central figure.

In Swedish corporate life, Fredrik is seen as a counterpart to the Wallenberg sphere: quieter and more domestic, with a strong bias toward property, banks, and industrials rather than global private equity.

L E Lundbergföretagen as family office:

L E Lundbergföretagen is effectively the family office, but in listed form: it is an investment company controlled by the Lundberg family, yet traded on Nasdaq Stockholm.

The company’s strategy emphasizes financial strength, low risk of permanent capital loss, and active board‑level involvement in a relatively small number of holdings.

A wholly‑owned subsidiary, Lundbergs Fastigheter, manages a significant Swedish commercial and residential property portfolio in cities like Stockholm, Gothenburg and Norrköping, providing stable, cash‑flowing ballast to the more market‑sensitive listed equities.

This structure forces mark‑to‑market transparency and a discipline around payout policy that is closer to a public investment company than a private family office.

Style as capital allocators:

The family’s approach is long‑duration, low‑turnover, and governance‑focused: they take sizable minority stakes and exercise influence through chairs/board seats and nomination committees rather than frequent trading.

They prefer strong balance sheets, industrial “national champions” and banks, and tend to add through cycles, particularly in periods of Swedish market stress (e.g., post‑crisis recap situations in banks and industrials).

Real estate and core equity holdings are used in combination: property for stable, collateralizable cash flows; equities for compounded operational leverage in high‑quality businesses.

In the Industrivärden case, the Lundberg family uses Lundbergföretagen to hold a large block of Industrivärden, and then leverages Industrivärden’s blocks in Volvo, Sandvik, Handelsbanken, Essity, SCA, etc., creating a layered but still fairly transparent structure of industrial ownership in Sweden.

THE BUSINESS:

source: annual report 2025

Before continuing take in mind that the group decided go with four main business lines and in 2026 the reporting will be structured around the following business areas: Health & medical; Personal care; Consumer tissue; and Professional hygiene.

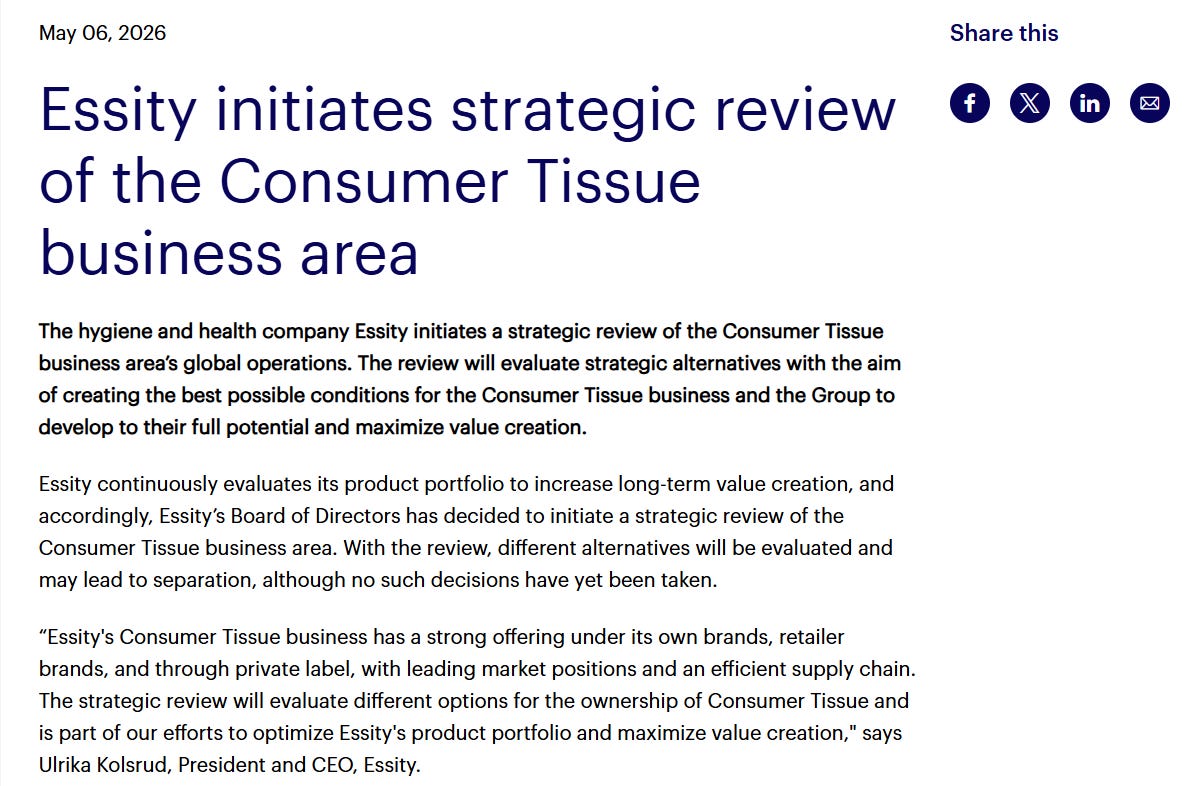

Another important caveat to take in mind is that the company issued and official statement about initiating a strategic review on the consumer tissue business:

source: https://www.essity.com/media/press-release/essity-initiates-strategic-review-of-the-consumer-tissue-business-area/4f1ae7af2e77f554/

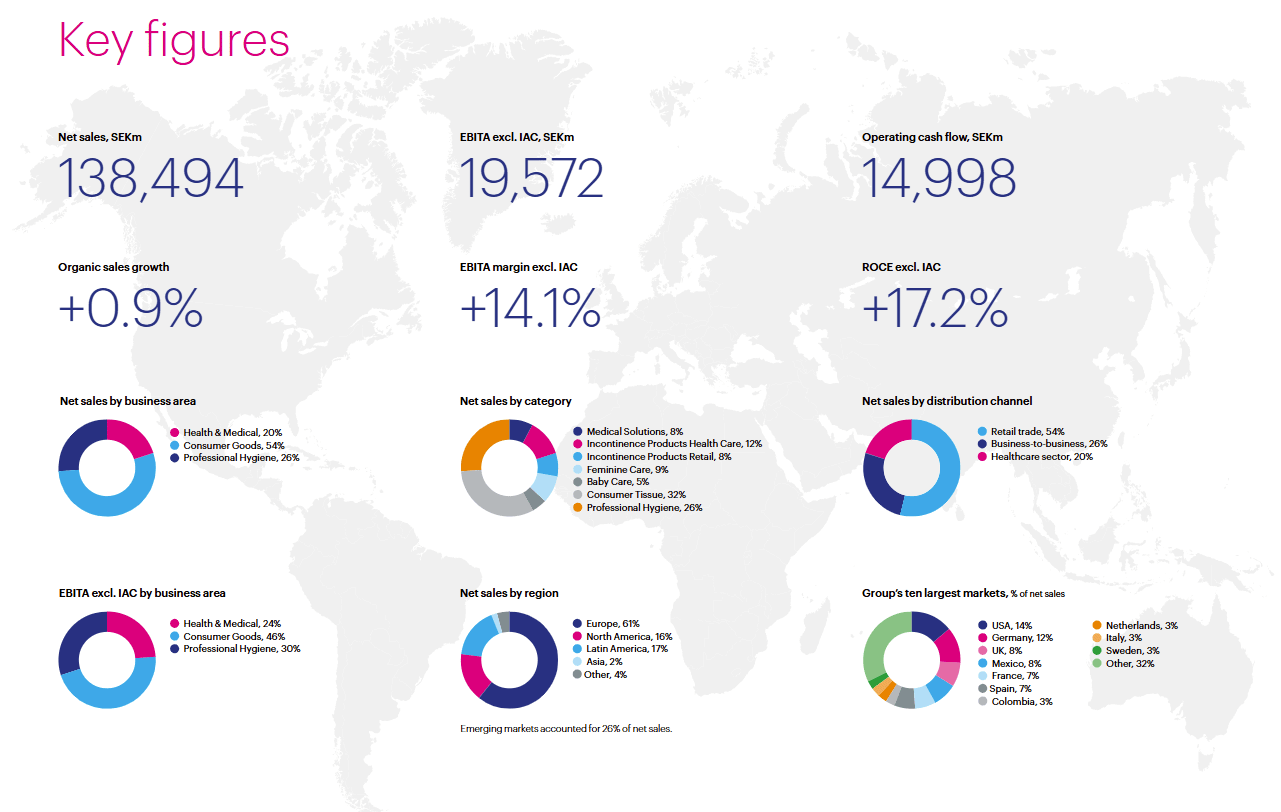

This is quite a diversified group.

There are 3 main business areas with consumer goods > 50% (54%) while the smaller business lines represent 20% for the health & medical and 26% for the professional hygiene line.

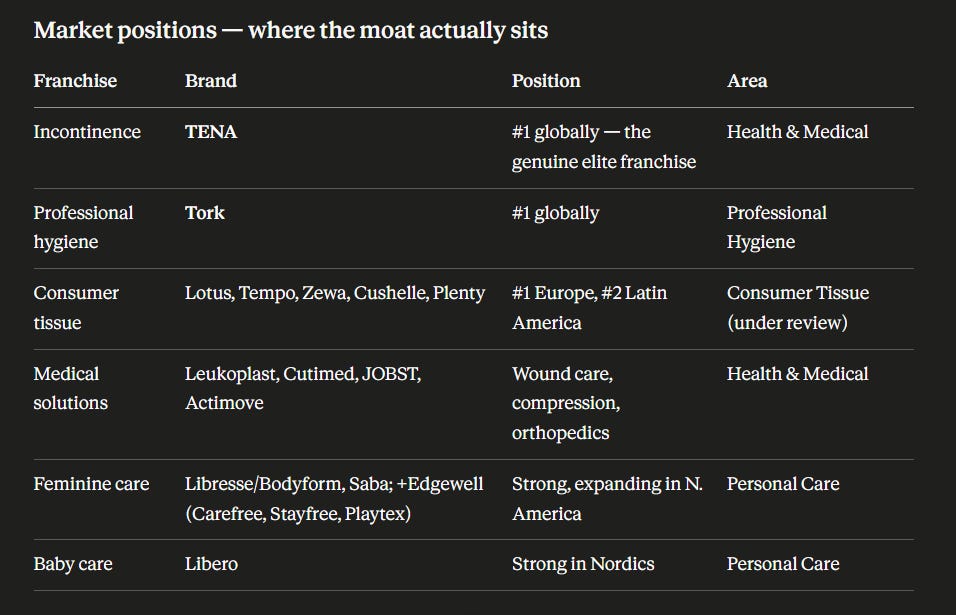

In terms of category of products there are two Tier I pillars - consumer tissue with 32% of sales and professional hygiene 26% of sales. The other categories - Incontinence products health care 12%; Feminine care 9%; Medical solutions 8%; Incontinence products retail 8% and baby care 5%.

Most of the sales go through retail channels - 54% of total sales. B2B account for 26% of sales and the remainder 20% go through the healthcare sector.

In terms of operating profit measured by EBITA - the distribution is somewhat more balanced. The consumer goods business area is by far the leader in sales but is less profitable in terms of margin. This line represents 54% of net sales but 46% of EBITA. Professional hygiene accounts for 26% of net sales but 30% of EBITA. Health & medical is 20% of net sales but 24% of EBITA.

In terms of geographic spread, sales are heavily tilted toward Europe. 61% of total net sales come from Europe.

On a country level the markets are very diversified. There is no single market with higher than 15% exposure. Biggest market is US with 14% weight. Second comes Germany with 12%, next is UK with 8%, Mexico also with 8%, France with 7%, Spain with 7%.

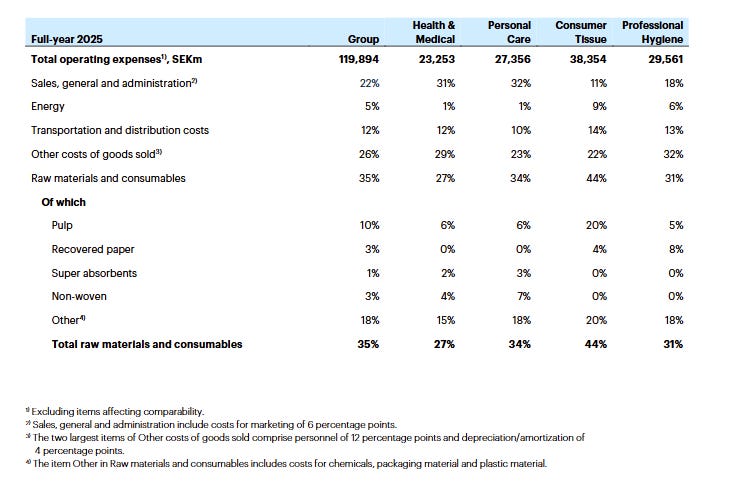

What about cyclicality? I think cyclicality can address different key drivers in a business. In terms of demand I think the cyclicality of Essity business is very low. The strongest cyclicality component of the business is nested in the cost structure - the cost of pulp/paper:

source: annual report 2025

Where the moat sits? This is a company focused on brands, so the strength of the brands and the market position they are commanding can give a valuable insight for us: