Is a Tailwind Good Enough?

Assystem is Europe's cleanest nuclear engineering pure-play, riding a multi-decade build-out. Three structural defects keep it out of the permanent portfolio.

I. Executive Verdict

Assystem is a clear and well-positioned nuclear-engineering franchise riding a genuine civilizational tailwind. The strategic narrative is one of the most coherent in European mid-cap industrials. The price is not punishing. But the framework verdict is unambiguous: this is not a custodial holding. Three structural defects disqualify it from custodial tier - an unaddressed founder succession, the €590M-net-debt Expleo overhang with 2027 maturities, and a free-share plan that has transferred material value from shareholders to management in 2024–2025. The thesis is a nuclear renaissance thematic exposure, not a multi-generational compounder.

II. Financial Snapshot

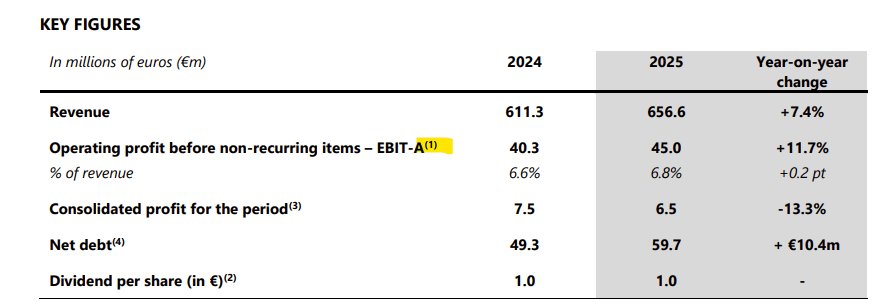

source: https://www.assystem.com/wp-content/uploads/2026/03/ASSYSTEM-Resultats-annuels-2025-CP-ENG-100326.pdf

One of the thigs that I don’t like in these numbers is the adjusted EBIT which is used as a headline profit number.

source: https://www.assystem.com/wp-content/uploads/2026/03/ASSYSTEM-Resultats-annuels-2025-CP-ENG-100326.pdf

Always focus on financial reports and not on headline numbers or some kind of adjusted summary tables.

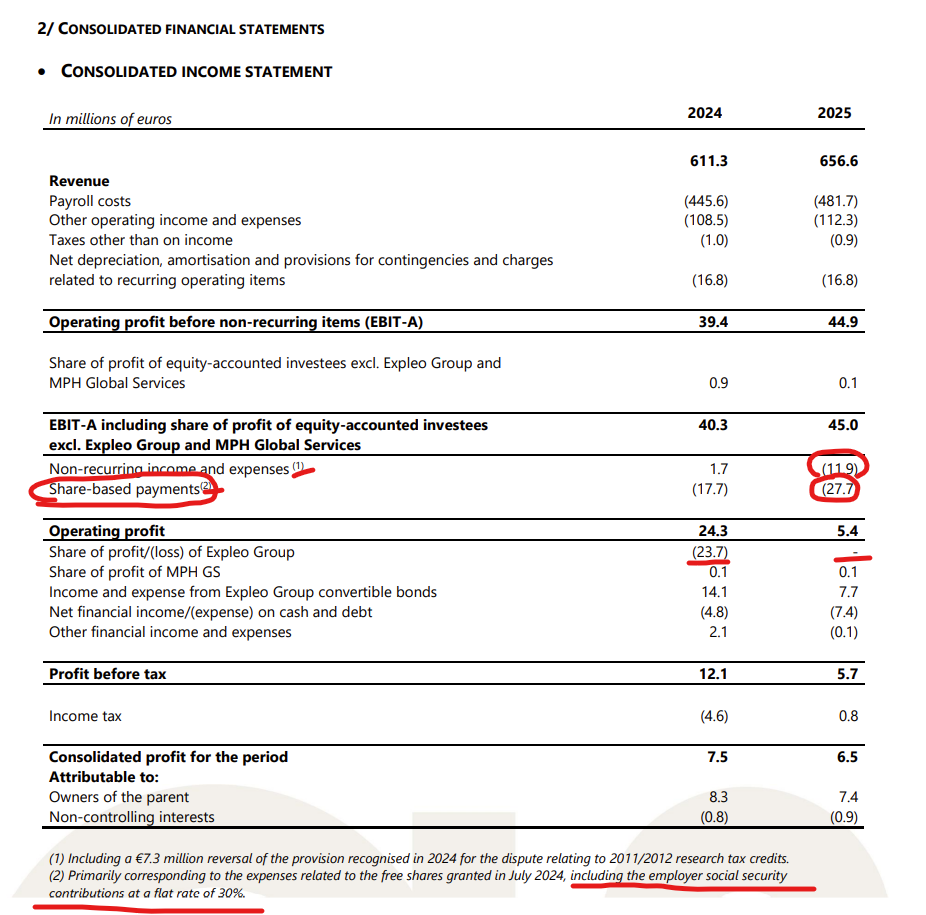

source: https://www.assystem.com/wp-content/uploads/2026/03/ASSYSTEM-Resultats-annuels-2025-CP-ENG-100326.pdf

Revenue is rising, “EBIT-A” is rising which can give us a healthy picture on the core operating business.

The two cautious moments I want to learn more about are facts and figures related to the Expleo Group and what is with the aggressive share-based-payments.

Who are Expleo Group?